I believe that we can substantially ease the public’s concern that monetary policy will become restrictive in the near to medium term and, hence, reduce the restraint in expanding economic activity. This can be done by clearly spelling out in our policy statements the conditionality of our dual mandate responsibilities. What should such a statement look like? I think we should consider committing to keep short-term rates at zero until either the unemployment rate goes below 7 percent or the outlook for inflation over the medium term goes above 3 percent. Such policies should enable us to make progress toward our mandated goals. But if this progress is too slow, then we should move forward with increased purchases of longer-term securities. We might even consider a regime in which we reevaluate our progress toward our policy goals and the rate of purchase of such assets at every FOMC meeting.

Let me note several aspects to this policy conditionality. As I just said, I subscribe to a 2 percent target for inflation over the long run. However, given how badly we are doing on our employment mandate, we need to be willing to take a risk on inflation going modestly higher in the short run if that is a consequence of polices aimed at lowering unemployment. With regard to the inflation marker, we have already experienced unduly low inflation of 1 percent; so against an objective of 2 percent, 3 percent inflation would be an equivalent policy loss to what we have already experienced. On the unemployment marker, a decline to 7 percent would be quite helpful. However, weighed against a conservative estimate for the natural rate of unemployment of 6 percent, it still represents a substantial policy loss. Indeed, weighed against a less conservative long-run estimate of the natural rate, it is a larger policy loss than that from 3 percent inflation. Accordingly, these triggers remain quite conservatively tilted in favor of disciplined inflation performance over enhanced growth and employment, and it would not be unreasonable to consider an even lower unemployment threshold before starting policy tightening.

I would also highlight that while I believe that optimal policy would be consistent with inflation running above our 2 percent target for some time, this policy does not abandon the 2 percent target for long-run inflation. Indeed, I would support combining this policy with a formal statement of 2 percent as our longer-run inflation target in conjunction with reaffirming our commitment to flexible inflation-targeting. Furthermore, I see a 3 percent inflation threshold as a safeguard against inflation running too high for too long and thus unhinging longer-run inflation expectations. It also is a safeguard against the kinds of policy errors we made in the 1970s. If potential output is indeed lower and the natural rate of unemployment higher than I currently think, then resource pressures would emerge and actual inflation and the outlook for inflation over the medium term would rise faster than expected. If this outlook for inflation hit 3 percent before the unemployment rate falls to 7 percent, then we would begin to tighten policy.

I understand that some may find such a policy proposal to be hard to understand, or even risky. But these are not ordinary times — we are in the aftermath of a financial crisis with massive output gaps, with stubborn debt overhangs and high degrees of household and business caution that are weighing on economic activity. As Ken Rogoff wrote in a recent piece in the Financial Times, “Any inflation above 2 percent may seem anathema to those who still remember the anti-inflation wars of the 1970s and 1980s, but a once-in-75-year crisis calls for outside-the-box measures.”[9] The Fed has done a good deal of thinking out of the box over the past four years. I think it is time to do some more.

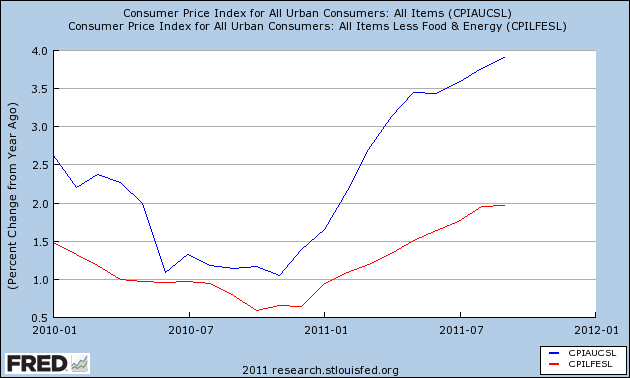

So basically he wants to increase our inflation target to 3% to allow us more leeway to reinflate the economy and get unemployment under control. There is only one problem, according to the latest CPI figures, inflation is already up by 3.9% over the last 12 months, up from less than 2% at the beginning of the year. I do realize of course that he is not thinking about actual CPI, but the statistical and non-real world subset that is considered "core" CPI, which is CPI less food and energy (let me know if you find anyone walking the street who can get by without food or energy expenditure). But as you can see from the graph below, even core CPI (the red line) is headed up and is already at the 2% target:

Even if the Fed did nothing more CPI could continue to drift higher by itself, possibly as high as Mr. Evans' new target of 3%. And the real CPI, the one you and I feel in our daily lives, could easily be north of 5-6%. How does that make any sense? And does he not remember QE2? There were few, if any, additional jobs created and all we got were higher commodity (food + energy) and stock prices. Employment just continued to stagnate, and this was after $600 billion was pumped into the economy. What Charles Evans wants is just a recipe for continued disaster.

No comments:

Post a Comment